Bitcoin

Bitcoin  Ethereum

Ethereum  BNB

BNB  XRP

XRP  Solana

Solana  TRON

TRON  Dogecoin

Dogecoin  Hyperliquid

Hyperliquid  Zcash

Zcash  Cardano

Cardano  Stellar

Stellar  Hedera

Hedera  Sui

Sui  Shiba Inu

Shiba Inu  Bittensor

Bittensor  World Liberty Financial

World Liberty Financial  Aster

Aster  Ripple USD

Ripple USD  Polkadot

Polkadot  Render

Render  Artificial Superintelligence Alliance

Artificial Superintelligence Alliance

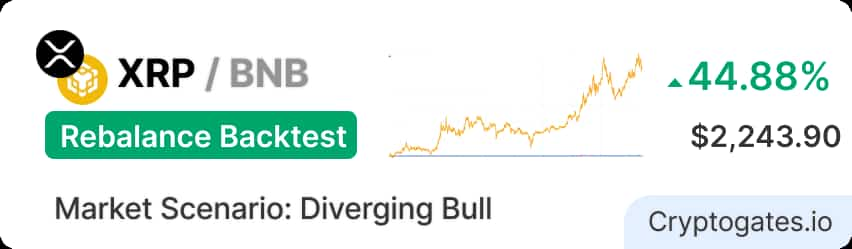

When One Asset Runs and the Other Walks, Rebalancing Has a Job to Do

XRP entered April 2025 at $2.13 — trading quietly while the broader market digested months of volatility.

By August 15, XRP closed at $3.08. That’s a 44.6% gain across 122 days. Not a parabolic moonshot — a sustained, grinding rally that rewarded patience and punished late buyers who chased the top.

BNB told a different story. It opened at $584.53 and closed at $627.81 — a steady +7.4% gain. Solid for a major chain token. But light years behind XRP’s pace.

The question we wanted to answer:

When two assets in the same portfolio diverge this aggressively, does a rebalance bot that systematically trims the winner and buys the laggard actually generate more value than holding both and doing nothing?

We ran a full 122-day backtest using real Binance OHLCV data to find out.

XRP — 50% TARGET

BNB — 50% TARGET

Strategy Parameters

How Each Setting Impacted Performance?

Every parameter had a job. In a diverging bull market, most of them did exactly what they were designed to do.

Parameter Impact Summary

| Parameter | Impact | The Logic (Why) |

|---|---|---|

| 60/40 XRP/BNB Allocation | 📈 Amplified gains | Higher XRP weight captured the stronger runner |

| 5% Ratio Threshold | 🎯 Minimal friction | Triggered only 3 swaps — let winners run longer |

| By Coin Ratio Logic | ⚖⚖️ Systematic profit-taking | Trimmed XRP gains to rebalance into BNB |

| No Time Rebalance | 🛡️ Zero noise tradesg | Eliminated fee drag from arbitrary time triggers |

| 0.08% Fee / Conversion | ⚡ Near-zero cost | $4.58 total fees on $5,000 over 4 months |

3 Swaps. $4.58 in Fees. +$2,243.90 in Profit.

📝 The math that matters

💰 The Bottom Line

This strategy delivered $2,243.90 net profit on $5,000 capital — a 44.88% four-month return. Against the HODL benchmark of 43.22%, the rebalancing edge was +1.66%, translating to approximately $82.90 in additional profit versus doing nothing. Annualized, a sustained 44.88% quarterly pace projects to roughly 179% annually — but that assumes another XRP-level divergence event, which is an aggressive forward assumption.

⚡ Efficiency of Low Activity

Three swaps across 122 days is a masterclass in restraint. The 5% threshold kept the bot quiet during noise and only fired when the allocation genuinely drifted. Each swap carried an average cost of just $1.53 at OKX’s 0.08% rate. Total fee drag: $4.58 — just 0.2% of gross profit. This is fee efficiency at its best.

🛡️ The HODL Edge in Context

The +1.66% edge over passive holding looks modest. But reframe it: the bot extracted $82.90 of additional profit through 3 automated swaps, at a total cost of $4.58 in fees. That’s an $18.06 return per dollar spent on fees. In a bull market where both assets rise, a rebalancing edge of any size is genuine alpha — the bot didn’t just ride the market, it actively improved on it.

Here comes our A/B/C strategies quick comparison:

| Variant | Threshold | Trades | ROI % | P&L (USDT) |

|---|---|---|---|---|

| AThis Playbook | 5% | 3 | 44.88% | $2,243.90 |

| B | 2% | 11 | 44.17% | $2208.64 |

| C | 2% | 13 | 43.86% | $2,192.93 |

Variant A won — and it did the least work. With only 3 swaps versus Variant C’s 13, it generated $51 more in profit while paying a fraction of the fees.

The pattern here is important: in a trending bull market where XRP is consistently outperforming BNB, frequent rebalancing means repeatedly trimming the winner. Every extra swap sold XRP gains to buy BNB, which was rising more slowly. The 5% threshold lets XRP run further before trimming, capturing more of the rally. Tighter thresholds (Variant B and C) acted like an anchor on the best-performing asset.

More swaps ≠ , more profit. In a diverging bull market, patience beats activity.

What the results are really telling you.

✅ what worked

Fee management was exceptional. Three swaps at 0.08% generated $4.58 total — less than 0.1% of the final portfolio value across a 4-month backtest. The 5% ratio threshold is the real hero here.

By requiring a meaningful drift before triggering a rebalance, it avoided trimming XRP too early during its rally. The March 4 rebalance — the first triggered swap — caught a genuine allocation drift and repositioned the portfolio cleanly without disrupting the XRP uptrend. Restraint was the edge.

⚠️What didn't work

The 60% XRP tilt, while profitable, carried concentration risk. Had XRP reversed after the first rebalance, the portfolio would have held an outsized XRP position at elevated prices.

BNB’s +7.4% gain contributed only ~$148 of the $2,243.90 total — 6.6% of all profits came from a 40% allocation. The rebalance logic also systematically sold XRP to buy BNB every time the drift triggered, meaning the bot was always buying the underperformer. If BNB had declined instead of rising modestly, the rebalancing would have compounded losses on that leg.

💡 The key insight

Rebalancing doesn’t predict winners. It harvests the gap between them.

The bot didn’t know XRP would run 44.6%. It didn’t need to. Its job was to monitor the allocation ratio and, when XRP’s gains pushed the portfolio beyond 5% of target, sell a slice of XRP and buy BNB. Every swap was mechanically selling high on the stronger asset and buying low on the weaker one.

In a scenario where assets eventually mean-revert (or where both keep trending), this extraction of spread is pure structural alpha.

The real risk isn’t the bot — it’s the pair. If BNB had broken down structurally (not just underperformed, but fallen sharply), every rebalance swap would have increased exposure to a genuinely declining asset. Choose pairs where both assets have fundamental floors. This setup’s edge lives in divergence, not destruction.

🚩 Watch out for - a potential red flag

The 60% XRP concentration is a double-edged sword.

During this backtest, XRP rose 44.6%, and the tilt paid off generously. But “60% in one altcoin” is a high-conviction bet. If XRP had reversed mid-period sharply, say, a regulatory headline or a market-wide correction, the rebalance bot would have kept buying XRP on the way down, increasing exposure to a falling asset with every triggered swap.

The mandatory end-date conversion also matters: it crystallizes every unrealized position into cash at close. A three-month snapshot may catch a temporary dip and lock in a lower value than the mid-period peak.

Before deploying this exact configuration, ask: if XRP drops 30% from entry without recovering in the backtest window, am I comfortable holding a 60% position all the way down? If not, reduce XRP allocation to 50% or tighten your rebalance threshold review cadence.

Overall Performance Score, Strengths and Limitations

Strong Divergence Rebalance Strategy

+44.88% in 122 days on a pair where only one asset ran hard. A +1.66% edge over passive HODL with just 3 swaps and $4.58 in fees demonstrates clean execution. The strategy did exactly what a rebalance bot is supposed to do: systematically harvest the spread between two assets without emotional interference.

🧭 What this strategy does well

- +1.66% edge over pure HODL ($82.90 extra profit)

- Exceptional fee efficiency: $4.58 on $5,000 over 4 months

- Only 3 swaps — minimal friction, minimal noise

- 5% threshold let the winner run before trimming

🚫 What went wrong this month

- 60% altcoin concentration carries significant single-asset risk

- Rebalancing edge is modest (+1.66%) — the bulk of profit was simply market beta

- End-date USDT conversion crystallizes all unrealized positions at close

- Strategy breaks in a scenario where the dominant asset reverses sharply post-rebalance

Quick Takeaways

✔ Less rebalancing beats more — Variant A’s 3 swaps outperformed Variant C’s 13 trades

✔ Divergence is the engine — the XRP/BNB performance gap created the rebalancing opportunity

✔ Fee rate at 0.08% is nearly invisible — low-fee exchanges are non-negotiable for this strategy

✔ 5% threshold = patience — let the ratio drift meaningfully before trimming winners

✔ Both assets must have upside — if BNB had fallen, this backtest would look very different

How did passive HODL compare?

If you had simply bought $5,000 of XRP and BNB on April 15, 2025 at $2.13 and $584.53 and held to August 15, here’s how it compares:

The gap between strategies: $2,243.90 − $2,161.00 = +$82.90 in favor of the rebalance bot.

That’s $82.90 in additional profit, generated by 3 automated swaps costing $4.58 in total fees. The net efficiency of the rebalancing activity — profit generated minus fees paid — is $78.32 of pure alpha. In a market where both assets rose, that edge came entirely from the systematic harvest of allocation drift.

Before you run this playbook, check these off.

Before deploying this strategy, verify every item below. Do not skip items because market conditions “look similar” to April 2025.

🧠 Market Suitability Matrix

| Market Condition | Rating | Strategic Notes |

|---|---|---|

| One asset strongly outperforms, other consolidates | ★★★★★ ideal | Harvest spread at each 5% drift trigger |

| Both assets sideways / choppy with oscillation | ★★★★★ Ideal | Consistent rebalancing captures small ratio swings |

| One asset dips then recovers, other holds | ★★★★☆ Good | Buy the dip automatically; profit on recovery |

| Both assets in a mild bull market (similar pace) | ★★★☆☆ Moderate | Reduced divergence = fewer triggers = less alpha |

| One asset strongly outperforms and keeps running | ★★☆☆☆ Risky | Repeatedly trimming the winner limits upside capture |

| Both assets in steep decline | ★☆☆☆☆ Poor | Rebalancing redistributes losses; no spread to harvest |

| One asset in structural breakdown | ★☆☆☆☆ Poor | Bot systematically buys the falling asset all the way down |

How to tune this playbook for different scenarios.

Disclaimer: All data sourced from CryptoGates Rebalance Backtest Bot. Results are historical simulations using Binance 1-minute OHLCV data. Past backtest performance does not guarantee future live trading results. DYOR.

Battle-Test Your Strategy

Before the Market Does.

Eliminate guesswork with institutional-grade backtesting for DCA, Grid, and Rebalance bots. Real historical data. Real-world results.